Hippo Insurance's AI Home Strategy: IoT, Smart Home Data, and the Conversational Risk Interview

TL;DR

Hippo Insurance pioneered the smart-home-as-insurance-policy model, bundling Notion, Roost, SimpliSafe, ADT, and Kangaroo IoT devices into homeowners coverage to detect water leaks, freeze events, and intrusions before they become claims. The carrier has shipped more than 500,000 sensors, reports roughly 25% lower water-loss frequency in instrumented cohorts, and in April 2026 launched "Clara from Claims," a 24/7 conversational AI first-notice-of-loss (FNOL) agent the company expects to handle more than 70% of new claims digitally. Hippo's architecture targets a 30–35% increase in claims volume without adding adjuster headcount, with average initial customer contact now under two hours. But the IoT layer only sees what sensors see — it does not capture move-in context, life events, renovation plans, or the messy "why" detail that drives accurate underwriting and clean FNOL files. That is the conversational AI gap, and carriers that already win on telemetry will compound their lead by adding AI-led customer interviews at onboarding, renewal, and FNOL.

Hippo's Bet: The Smart Home Is the Underwriting Signal

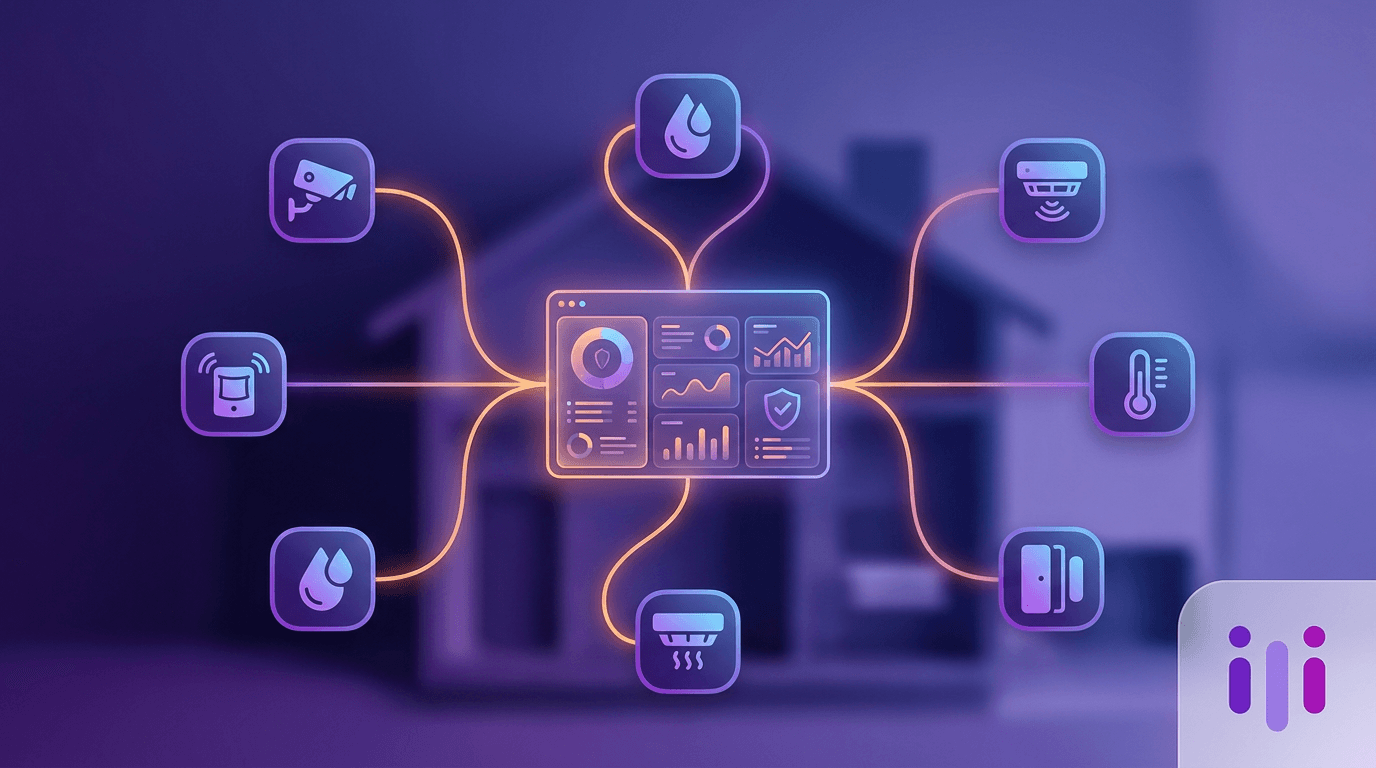

Hippo Insurance Services launched in 2015 on a thesis most legacy carriers found uncomfortable: homeowners insurance should prevent losses, not just pay for them. By 2017 it had operationalized that thesis through the industry's first IoT-bundled policy, partnering with Roost to ship every new policyholder a free smart water leak detector. That partnership turned into a portfolio: Notion multi-purpose sensors, a 7-piece SimpliSafe alarm kit with two water sensors, an ADT pro install/monitoring tier, and Kangaroo entry sensors. Today Hippo says it runs the most widely adopted smart home program in homeowners insurance, with 500,000+ sensors deployed and average annual customer discounts of $64 (self-monitored) to $91 (pro-monitored).

This is materially different from the standard carrier AI stack. Most home insurers treat AI as back-office plumbing for cat modeling, fraud detection, and document OCR. Hippo treats the home itself as a sensor surface. Critically, Hippo deliberately structured the program so sensor data reports to the homeowner, not the carrier — the only signal flowing back is whether the kit remains active. For a vendor-neutral view of this stack, see our 2026 state of AI customer communications in insurance.

The Hippo Smart Home Stack at a Glance

The pattern is consistent: capture a discrete physical event, route the alert to the homeowner, and use the program's existence as a soft underwriting signal. There is no rich behavioral telemetry flowing back to the carrier — a privacy-protective design that, by accident, leaves a large amount of valuable risk context on the table.

The Conversational Risk Interview Gap

Sensors capture events. They do not capture intent, context, or judgment.

Consider the data Hippo's sensor stack will never see:

- A policyholder is renovating the kitchen next month and adding a dishwasher on a previously dry circuit. (Increased water risk.)

- The home was just listed as a weekend short-term rental. (Increased liability and occupancy risk.)

- The basement was finished last year with no permit. (Mis-classified replacement value.)

- A claim is being reported and the homeowner says, "I think the water came from upstairs but I'm not sure" — the FNOL agent needs to probe, not present a dropdown.

These signals do not show up on a sensor. They show up in conversation. Carriers have tried to capture them with onboarding forms, renewal questionnaires, and IVR phone trees, all of which fail at exactly the moments where the customer needs to explain something messy. Forms flatten "it depends" into a dropdown that doesn't fit. Phone trees route on hard-coded keywords. This is why so many home claims get re-opened or under-reserved — and why we have written about the anti-pattern in why AI-first cannot start with a web form and why static intake forms kill conversion rates. An AI-led risk interview probes vague answers, branches on life events, and captures structured detail in the homeowner's own words — the layer Hippo's IoT-first strategy points toward but does not yet own.

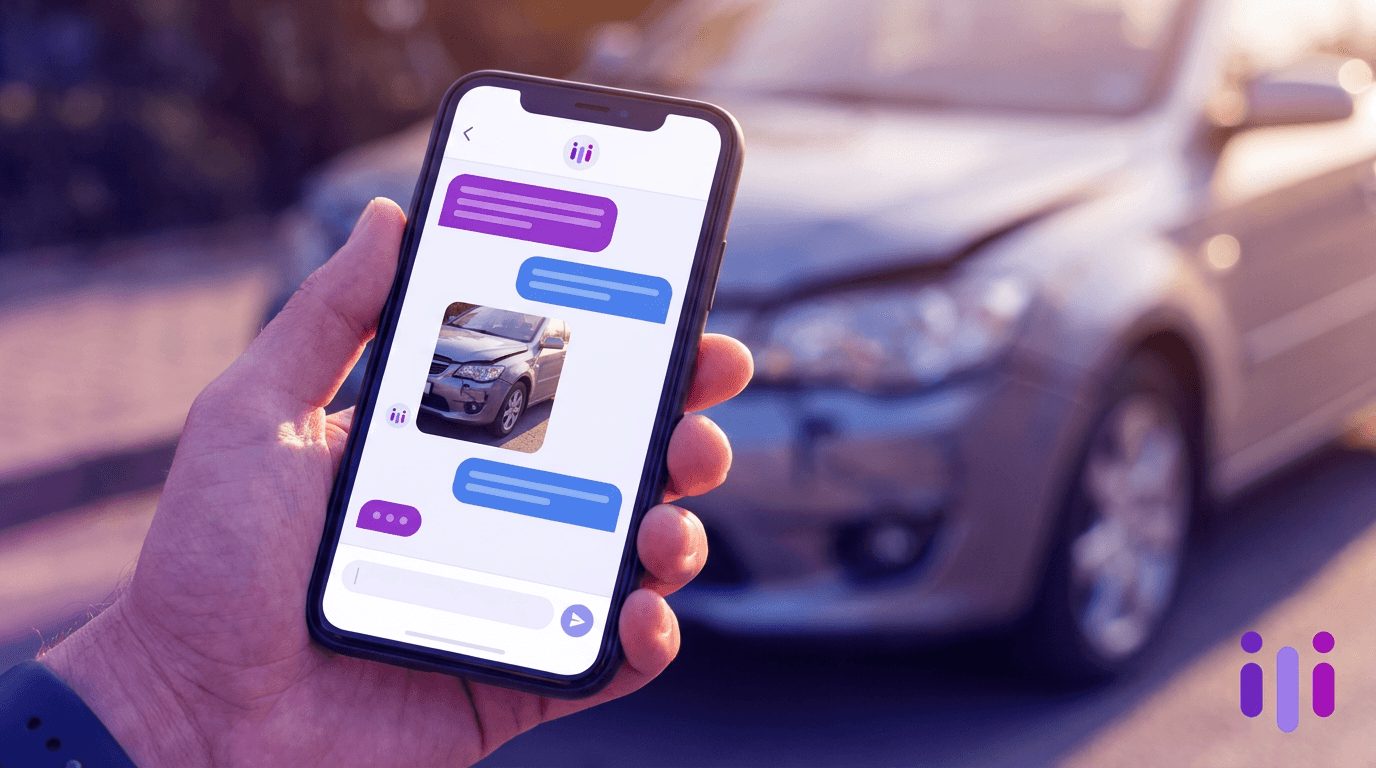

Clara from Claims: Hippo's First Conversational Move

In April 2026 Hippo announced "Clara from Claims," a 24/7 conversational AI agent that runs a fully digital FNOL experience. Per the company's own announcement, the architecture is designed to support a 30–35% increase in claims volume without adding headcount, has reduced average initial contact to under two hours, and is expected to handle more than 70% of new claim filings digitally.

This matches a broader carrier pattern we have tracked across Lemonade's AI claims model and the 2026 AI customer communications roadmap for insurers: replace the IVR + adjuster phone-tag loop with a digital FNOL conversation, then route to a human only when judgment is required.

Clara is the right architectural move. The open question is how far Hippo extends it. FNOL is the obvious starting point — but the same conversational layer pays off harder at three earlier moments: move-in onboarding (first 30 days, when homeowners are most willing to disclose detail), renewal context ("what changed in the last year?" — always answered "nothing" on a form), and mid-policy life events (renovation, new occupant, short-term rental — all under-reported, all material to risk). Hippo's IoT layer cannot ask any of these questions. A conversational AI layer can.

Why Sensor Data + Conversational AI Compound

Telemetry and conversation answer different questions.

Carriers like Hippo are uniquely positioned here. They already own the sensor surface. Adding a conversational layer at onboarding, renewal, and FNOL turns each event the IoT detects into a structured story — feeding underwriting, claims, and customer success simultaneously. The same logic underpins the complete guide to AI-powered customer experience and what AI-native customer engagement actually means.

What Other Home Carriers Should Take From Hippo

Most home insurers will not replicate the full Hippo IoT investment — the device economics, partner stack, and operational lift are non-trivial. But every home carrier and broker can copy the conversational layer, which is where the marginal ROI is highest in 2026.

The practical sequence:

- Replace the new-policy intake form with an AI-led move-in interview. Cover occupancy, renovations, prior claims, pets, short-term rental use, and mitigation devices. Capture structured fields plus verbatim quotes for the underwriting file.

- Replace the renewal questionnaire with a 90-second renewal conversation. Probe on what changed and re-rate from the result.

- Layer a digital FNOL agent over the claims phone queue. Route to human adjusters only when judgment, fraud, or large-loss indicators trigger.

- Feed every conversation back into a single VOC repository. Patterns across thousands of move-in interviews surface emerging risk segments before any individual claim does — the same logic that makes voice of customer programs valuable in horizontal SaaS.

This is the AI for insurance agencies in 2026 playbook that mid-market carriers and brokerages are now operationalizing. It does not require sensor hardware — just a conversational interview surface that replaces the form fields no homeowner reads carefully, with a router that hands edge cases to a human.

Where Perspective AI Fits in the Carrier Stack

Perspective AI is the customer interview layer that sits where Hippo's IoT layer cannot reach — replacing forms with AI-led conversations that probe, follow up, and capture the "why" behind every onboarding, renewal, claim, and policy change. Our interviewer agent and concierge agent cover AI-led conversational intake for new policies, renewal interviews on what changed in the last 12 months, FNOL companion interviews that gather structured incident detail, and voice of customer programs across the book to surface emerging risk segments. For carriers already running an IoT program like Hippo's, this is additive, not competitive — the sensors stay where they are; the conversation layer does the work no sensor can do.

Frequently Asked Questions

What does Hippo Insurance's AI strategy actually cover?

Hippo Insurance's AI strategy spans three layers: a smart home IoT program with 500,000+ deployed sensors from Notion, Roost, SimpliSafe, ADT, and Kangaroo; an Opterrix-powered weather and risk intelligence platform for catastrophe response; and "Clara from Claims," a conversational AI FNOL agent launched in April 2026 designed to support 30–35% claims-volume growth without adding adjusters. Hippo's stated direction is an "agentic AI workforce" supporting human adjusters from FNOL through audit.

How does Hippo use IoT and smart home data in homeowners insurance?

Hippo bundles smart home sensors into new homeowners policies to detect water leaks, freeze events, smoke alarms, and intrusions before they become claims. Sensor data reports to the homeowner, not to Hippo — the only signal flowing back to the carrier is whether the kit remains active, which determines discount eligibility. Hippo reports about 25% lower water-loss frequency in cohorts with active smart home programs and offers $64–$91 in average annual premium discounts.

Why isn't Hippo's IoT program enough on its own?

Hippo's IoT program is a sensor surface — it captures discrete physical events like leaks, freezes, smoke, and intrusion, but not intent, life events, occupancy changes, renovation plans, or the verbatim "why" detail behind a claim. Those signals only surface in conversation. Forms and IVR phone trees fail at this because they flatten messy answers into dropdowns and keywords. Conversational AI interviews close the gap by probing and branching on context at onboarding, renewal, and FNOL.

What is Clara from Claims and how does it work?

Clara from Claims is Hippo's 24/7 conversational AI agent for first notice of loss (FNOL), launched in April 2026. It runs a fully digital intake conversation that captures incident detail, sequence of events, and policyholder context, then routes to human adjusters when judgment is required. Hippo expects Clara to handle more than 70% of claim filings digitally, has cut average initial customer contact to under two hours, and projects the architecture supports a 30–35% increase in claims volume without adding adjuster headcount.

How can other home insurance carriers copy Hippo's playbook without the sensor program?

Other home carriers can copy the high-ROI half of Hippo's playbook — the conversational AI layer — without replicating the IoT hardware investment. The sequence: replace the new-policy intake form with an AI-led move-in interview, replace the renewal questionnaire with a 90-second conversation, layer a digital FNOL agent over the claims queue, and aggregate all conversations into a single VOC repository. This delivers most of the conversational ROI without shipping sensors.

Where does conversational AI fit alongside an IoT-based insurance product?

Conversational AI sits at the human moments an IoT sensor cannot reach: policy onboarding, mid-term life events, renewal context, and FNOL narrative capture. Sensors answer "what is happening in the home right now"; conversational AI answers "why, what changed, and what should the carrier do about it."

The Takeaway

Hippo Insurance's AI home strategy is the most fully-realized example of carrier IoT in homeowners insurance — a smart home program at real scale, demonstrable claim-frequency reduction, and now a conversational FNOL agent in production. The next phase for any carrier following Hippo's lead is closing the conversation gap: replacing forms and IVR with AI-led customer interviews at the moments sensors cannot reach. Move-in interviews capture context. Renewal interviews catch changes. FNOL interviews build the file. Together they convert raw sensor telemetry into structured risk intelligence — where the next decade of home insurance underwriting accuracy will be won.

To layer conversational customer interviews on top of your existing telemetry and claims stack, start a Perspective AI research project or explore the interviewer agent. The sensors caught the leak. The conversation tells you why.

More articles on Intelligent Intake

Allstate's AI Claims Strategy: What QuickFoto Claim and Conversational AI Mean for the Industry

Intelligent Intake · 13 min read

Geico's AI Chatbot Strategy: How the Auto Insurance Giant Is Replacing Forms with Conversations in 2026

Intelligent Intake · 11 min read

Next Insurance and the AI-First SMB Insurance Playbook: How Conversational Quoting Beats Form-Based Quoting

Intelligent Intake · 16 min read

Progressive's Snapshot and the Conversational AI Frontier: How Telematics Pioneers Are Replacing Survey Calls

Intelligent Intake · 12 min read

Root Insurance's AI Underwriting Bet: Behavior-Based Pricing and the Conversational Risk Interview

Intelligent Intake · 15 min read

State Farm's AI Roadmap: How the Largest US Insurer Is Modernizing Customer Experience in 2026

Intelligent Intake · 13 min read